Short GBP-JPY: Looking for JPY strength amid narrowing central bank divergences

Recent JPY weakness is an opportunity to long JPY on the crosses

Chief Investment Office14 Feb 2023

- BOJ and BOE stances are converging towards neutral from the respective dovish and hawkish extremes

- This favours a lower GBP-JPY going forward

- Opportunities to go short on GBP-JPY given recent JPY weakness amid BOJ governor uncertainty

- Look to enter a short GBP-JPY position near its 50-DMA at 160.90

- Targeting 155.00 and setting a stop-loss at 163.80

Photo credit: iStock

Read More

BOJ and BOE stances are converging towards neutral from the respective dovish and hawkish extremes.

- The identity of the new Bank of Japan (BOJ) governor has been a matter of media and market speculation over the past two weeks, leading to heightened volatility in the USD-JPY during this period. The choice has settled down to ex-BOJ board member, Kazuo Ueda, who is deemed to be less dovish than the previous front-runner, the current Deputy Governor Masayoshi Amamiya.

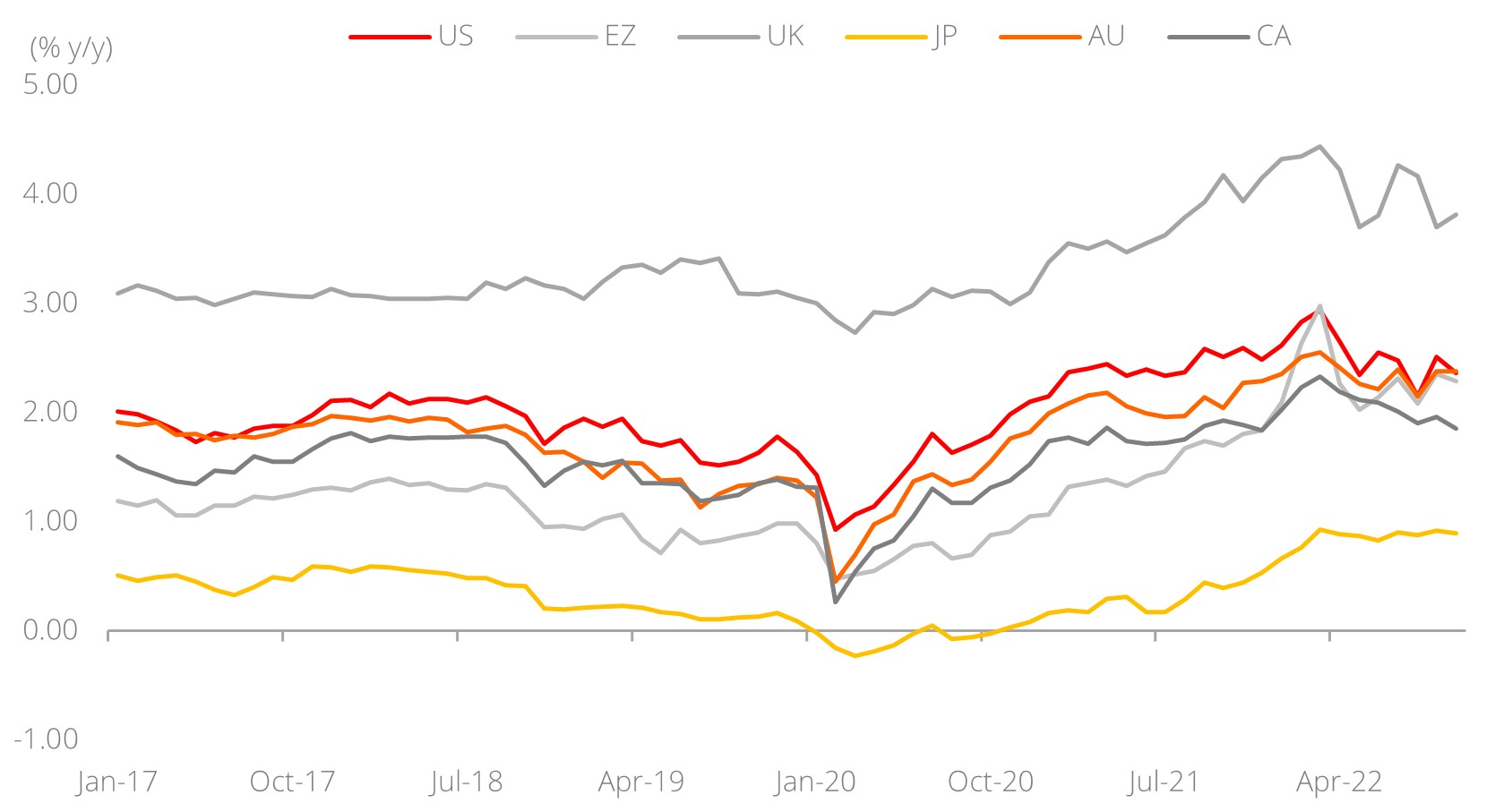

- The USD-JPY reacted lower when Ueda was first floated as a candidate on 10 Feb. However, the move was pared by the start of this week (ending 17 February). Putting aside the short-term noise, the longer-term bias for the BOJ to shift towards neutral from its dovish extreme in 2023 should be unchanged. The BOJ has historically stayed at the dovish extreme to spur its inflation towards the 2.0% target – this dynamic is less pressing now, with the headline CPI inflation in Japan now pushing 4.0% y/y (see Chart 1 below). The BOJ has room to be less dovish in 2023.

- This should eventually translate to looser yield curve control (YCC) parameters at the BOJ, and therefore higher back-end Japanese Government Bond yields. Expect this to eventually flow through to a stronger JPY this year.

Chart 1: Headline CPI inflation across major economies

Source: Bloomberg, DBS

- On the flipside, the Bank of England (BOE) has been hawkish, pencilling in 390 bps of rate hikes since the start of this rate hike cycle. The cumulative rate hikes are now forecasted to depress UK inflation towards 4.0% y/y in 2023 from a high of 11.1% y/y in October 2022.

- With inflation potentially “turning the corner”, the bias at the BOE is now leaning towards a rate pause. Some members in the BOE’s Monetary Policy Committee are cautioning against “doing too much” on rate hikes (Huw Pill) and commenting that the current policy rate 4.0% is “too high” (Silvana Tenreyro). This suggests that the balance of risk for the BOE will be towards being less hawkish, and more neutral, going forward.

- With the BOE and BOJ moving towards neutral from opposite ends of the spectrum, we have the central bank divergence narrowing in favour of a softer GBP and stronger JPY. This favours a short GBP-JPY idea.

Recent spike in the GBP-JPY amid the uncertainties over the BOJ governor is an opportunity to enter short at favourable levels.

Chart 2: GBP-JPY weekly chart from 1Q19

Source: Bloomberg, DBS

- The GBP-JPY has stayed in a multi-month uptrend channel (1) that has persisted since May 2020. This trend channel was broken in late December 2022 (2) amid JPY strengthening, and the pair has since been consolidating between the 50- and 100-WMAs. From a long-term perspective, coming off an uptrend channel typically signals a potential reversion into a downtrend. Note that the weekly moving average convergence/divergence is also pointing to a growing downside momentum (3).

Chart 3: GBP-JPY daily chart

Source: Bloomberg, DBS

- Since breaking lower from the uptrend channel, the GBP-JPY has mostly kept within the 156.00 – 161.80 consolidation range (4a) (4b). The recent JPY weakness has taken the pair higher towards the top end of the recent range, but it was capped by the 50-DMA (160.94) (5).

- Considering the fundamental and technical angles, we believe there is an opportunity to explore a short GBP-JPY idea. We recommend the following parameters:

- Entry: 160.90 – leaning against the 50-DMA resistance.

- Target: 155.00 – below the recent range lows of 156.00.

- Stop-loss: 163.80 – above the 100- and 200-DMA resistances (6).

Download the PDF to read the full report.

Topic

Sanggahan

PT Bank DBS Indonesia (“DBSI”) berizin dan diawasi oleh Otoritas Jasa Keuangan, serta merupakan peserta penjaminan Lembaga Penjamin Simpanan. Informasi di dalam publikasi ini diterbitkan oleh DBSI. Informasi ini berlandaskan pada informasi yang diperoleh dari sumber yang diyakini dapat diandalkan, tetapi DBSI tidak membuat pernyataan atau jaminan, tersurat maupun tersirat, sehubungan dengan keakuratan, kelengkapan, aktualitas, atau kebenaran untuk tujuan tertentu. Pendapat yang diungkapkan dapat berubah tanpa pemberitahuan. Setiap rekomendasi yang terkandung di sini tidak berkaitan dengan tujuan investasi secara spesifik, situasi keuangan dan kebutuhan khusus dari penerima tertentu. Informasi ini diterbitkan hanya untuk informasi penerima dan tidak akan diambil sebagai pengganti pelaksanaan penilaian oleh penerima yang harus mendapatkan nasihat hukum atau keuangan terpisah. DBSI atau individu yang terkait dengan DBSI tidak bertanggungjawab atas kerugian langsung, khusus, tidak langsung, konsekuensial, insidental, atau kehilangan atau kerugian lain apa pun yang timbul dari penggunaan informasi apa pun di sini (termasuk kesalahan, kelalaian atau kekeliruan pemberian pernyataan di sini, lalai atau lainnya) atau komunikasi lebih lanjut, bahkan jika DBSI atau orang lain telah diberitahu tentang kemungkinannya. Informasi di sini tidak dapat ditafsirkan sebagai penawaran atau permintaan penawaran untuk membeli atau menjual surat berharga, kontrak berjangka, opsi atau instrumen keuangan lainnya atau untuk memberikan saran atau layanan investasi. DBSI, direktur, pejabat, dan/atau karyawan dapat memiliki posisi atau kepentingan lain dan dapat mempengaruhi transaksi dalam sekuritas/surat berharga yang disebutkan di sini dan juga dapat melakukan atau berupaya melakukan perantaan, investasi perbankan dan layanan perbankan atau keuangan lainnya untuk perusahaan-perusahaan ini. Informasi di sini tidak dimaksudkan untuk disebarluaskan kepada, atau digunakan oleh, orang atau badan mana pun di yurisdiksi atau negara mana pun dimana distribusi atau penggunaannya akan bertentangan dengan hukum atau peraturan. Sumber untuk semua grafik dan tabel adalah CEIC dan Bloomberg kecuali ditentukan lain.

©2024 PT Bank DBS Indonesia

PT Bank DBS Indonesia berizin dan diawasi oleh Otoritas Jasa Keuangan dan Bank Indonesia, serta merupakan peserta penjaminan Lembaga Penjamin Simpanan (LPS)